Why KLA Corporation Rose 14.3% in May – The Motley Fool

Founded in 1993, The Motley Fool is a financial services company dedicated to making the world smarter, happier, and richer. The Motley Fool reaches millions of people every month through our premium investing solutions, free guidance and market analysis on Fool.com, top-rated podcasts, and non-profit The Motley Fool Foundation.

Founded in 1993, The Motley Fool is a financial services company dedicated to making the world smarter, happier, and richer. The Motley Fool reaches millions of people every month through our premium investing solutions, free guidance and market analysis on Fool.com, top-rated podcasts, and non-profit The Motley Fool Foundation.

You’re reading a free article with opinions that may differ from The Motley Fool’s Premium Investing Services. Become a Motley Fool member today to get instant access to our top analyst recommendations, in-depth research, investing resources, and more. Learn More

You’re reading a free article with opinions that may differ from The Motley Fool’s Premium Investing Services. Become a Motley Fool member today to get instant access to our top analyst recommendations, in-depth research, investing resources, and more. Learn More

Positive earnings and a bounce-back month for tech propelled this semiconductor equipment provider's stock higher.

Shares of KLA Corporation (KLAC -0.41%) rose 14.3% in May according to data from S&P Global Market Intelligence. The semiconductor equipment company didn’t actually have much in the way of new news in May; however, it did report earnings in the last days of April. Unlike other semicaps that have missed earnings due to supply constraints, KLA actually beat for revenue and earnings. Yet with the outlook for semiconductor investment remaining positive even amid macro concerns, KLA found a bid after its valuation had fallen far enough.

In its fiscal third quarter, KLA posted $2.3 billion in revenue, up 27.2%, with adjusted (non-GAAP) earnings per share of $5.13. Both numbers beat analyst expectations. In the release, CEO Rick Wallace said, “The demand environment for KLA products and solutions remains robust amid a persistently challenging supply chain landscape, and we are focused on navigating this environment to consistently meet customer commitments and delivering on our long-term strategic objectives and financial targets.”

KLA is far and away the leader in process control equipment, which scans wafers and semiconductors for imperfections, making this equipment absolutely crucial to leading-edge semiconductor production. As more and more steps are required to produce leading-edge semiconductors, process control needs to be implemented at every step of the technically difficult process in order to ensure quality yields.

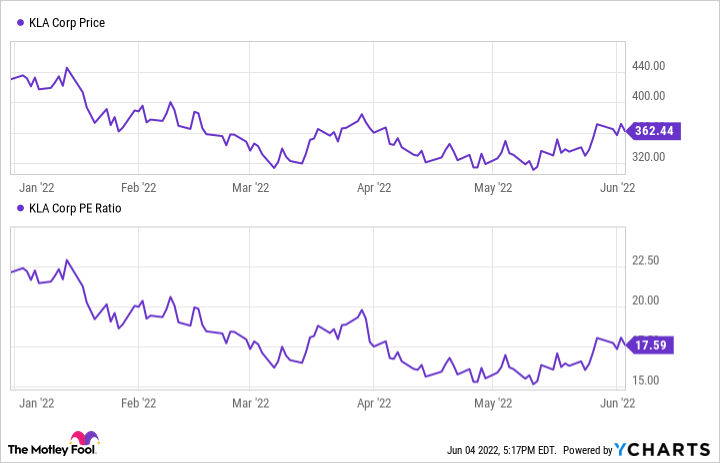

KLAC data by YCharts

Although this report came at the end of April, KLA continued to rise during May, likely because the stock just became too cheap relative to business performance. After falling to around 15 times earnings, the stock appeared to find its footing. Many beaten-down tech stocks seemed to find a bottom during the month, at least in the near term, and KLA was no different.

Image source: Getty Images.

Even at its current P/E ratio of 17.5, KLA seems cheap relative to its high-20% growth rate and high profitability. Although the semiconductor equipment industry has seen three straight years of growth and is known to be cyclical, there doesn’t seem to be much cyclicality in KLA’s results or outlook. In fact, this year should mark the seventh straight year of growth for KLA, even including the trade war downturn of 2019 and the COVID-19 year of 2020, when other types of equipment stocks saw mild declines.

In its shareholder letter, management also said, “The semiconductor industry has evolved to be significantly more strategic and has an increasingly less cyclical end market mix, with many fundamental drivers advancing the critical nature of semiconductors throughout the global economy.”

Semiconductor equipment stocks tend to trade at lower multiples than the broader overall market, due to their performance in past cycles; however, if KLA management turns out to be right, and the semiconductor industry becomes more of a steady growth industry, it’s possible shares could re-rate higher at some point. One might think after seven straight years of growth, KLA would have shed that reputation. While it’s true KLA does trade at a bit of a higher valuation than other equipment stocks in etch and deposition, its mid-teens multiple and low-teens forward multiple still seem far too low for a growth stock. Perhaps the market is beginning to come around.

Billy Duberstein has positions in KLA-Tencor. His clients may own shares of the companies mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.

Invest better with The Motley Fool. Get stock recommendations, portfolio guidance, and more from The Motley Fool’s premium services.

Making the world smarter, happier, and richer.

© 1995 – 2024 The Motley Fool. All rights reserved.

Market data powered by Xignite and Polygon.io.