Where Will Nvidia Stock Be in 3 Years? – The Motley Fool

Founded in 1993, The Motley Fool is a financial services company dedicated to making the world smarter, happier, and richer. The Motley Fool reaches millions of people every month through our premium investing solutions, free guidance and market analysis on Fool.com, top-rated podcasts, and non-profit The Motley Fool Foundation.

Founded in 1993, The Motley Fool is a financial services company dedicated to making the world smarter, happier, and richer. The Motley Fool reaches millions of people every month through our premium investing solutions, free guidance and market analysis on Fool.com, top-rated podcasts, and non-profit The Motley Fool Foundation.

You’re reading a free article with opinions that may differ from The Motley Fool’s Premium Investing Services. Become a Motley Fool member today to get instant access to our top analyst recommendations, in-depth research, investing resources, and more. Learn More

The company's top line is set to jump at a terrific pace over the next three years thanks to AI.

Nvidia (NVDA -0.71%) investors have seen their investments in this high-flying semiconductor company multiply substantially in the past three years. After all, Nvidia stock has shot up an impressive 576% during this period, which means that an investment of $1,000 in its shares three years ago is now worth more than $6,750.

The stock market has rewarded Nvidia investors with such handsome gains thanks to the impressive growth in its top and bottom lines.

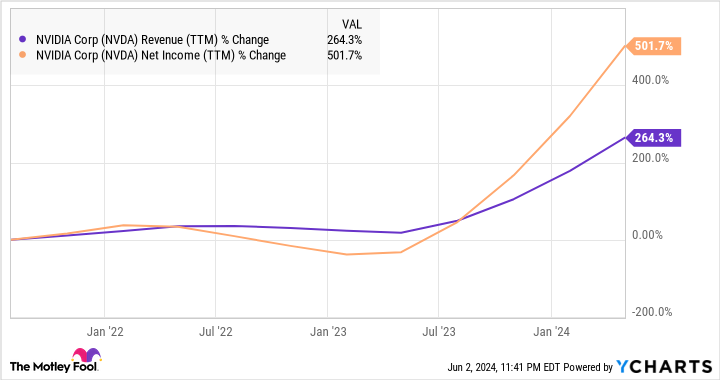

NVDA Revenue (TTM) data by YCharts

However, as the above chart indicates, Nvidia’s revenue and earnings growth started taking off only from the second half of 2023 once customers started lining up to buy its artificial intelligence (AI) chips. The good part is that this catalyst could help Nvidia stock sustain its impressive momentum over the next three years as well. Let’s look at the reasons why.

When Nvidia released its results for the first quarter of fiscal 2025 (which ended on April 28) last month, it became clear that it continues to remain the dominant player in the lucrative AI chip market.

The company’s revenue shot up a terrific 262% year over year to a record $26 billion. Non-GAAP earnings jumped 461% to $6.12 per share. The numbers were well ahead of what the market was forecasting. The positives didn’t stop there, as Nvidia’s revenue guidance of $28 billion for the current quarter means that its top line is set to more than double once again from the year-ago period’s reading of $13.5 billion.

The company managed to deliver such terrific growth even though its current generation of Hopper AI chips is about to be replaced with the new Blackwell generation. Management pointed out on the latest earnings conference call that it witnessed “strong demand” for the Hopper graphics processing units (GPUs).

The good part was that Nvidia was able to increase the supply of its previous generation H100 GPU so that it could fill more demand. However, the company also pointed out that the demand for its latest Hopper flagship — the H200 processor — was stronger than supply. Additionally, Nvidia is expecting that the demand for its Blackwell chips, which are already in production, will remain ahead of supply “well into next year.”

What this means is that the demand for Nvidia’s AI GPUs is so strong that the company is unable to manufacture enough chips. Even better, its competitors are unable to fill the supply void as Nvidia reportedly commands 60% of the advanced chip packaging capacity — which is required to produce AI chips — of its foundry partner. As a result, Nvidia continues to dominate the AI chip market with an estimated share of more than 95% as per some estimates.

The good part is that Nvidia’s foundry partner TSMC is set to expand its advanced chip packaging capacity at an annual rate of 60% through 2026. This bodes well for Nvidia, as it should ideally be able to manufacture more AI chips and reduce lead times for customers waiting to get their hands on the company’s hardware.

Higher production should ideally translate into more revenue growth and allow Nvidia to maintain its solid share of the AI chip market that’s expected to generate annual revenue of $400 billion in 2027 as compared to $45 billion last year, according to fellow chipmaker AMD.

We have seen that the market for AI chips is set to boom over the next three years. When combined with Nvidia’s outstanding market share in this space, it is easy to see why analysts are expecting its top-line growth to take off over that time frame.

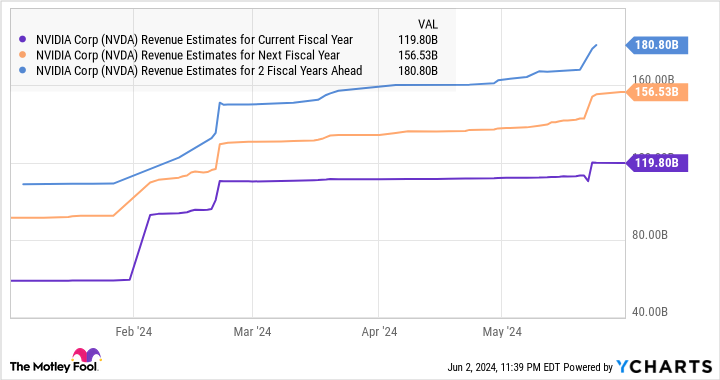

NVDA Revenue Estimates for Current Fiscal Year data by YCharts

Nvidia finished the previous fiscal year with just under $61 billion in revenue, and the chart above indicates that its top line is forecasted to nearly triple over the next three years. However, certain analysts are expecting Nvidia’s revenue to grow even faster by 2027 and outpace Wall Street’s expectations.

As such, there is a good chance that Nvidia will continue to remain a top growth stock over the next three years as well. With shares of the company now trading at 42 times forward earnings, which is in line with the U.S. technology sector’s average price-to-earnings ratio, buying Nvidia looks like a no-brainer considering the pace at which it is expected to grow over the next three years.

Harsh Chauhan has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Advanced Micro Devices, Nvidia, and Taiwan Semiconductor Manufacturing. The Motley Fool has a disclosure policy.

Invest better with The Motley Fool. Get stock recommendations, portfolio guidance, and more from The Motley Fool’s premium services.

Making the world smarter, happier, and richer.

© 1995 – 2024 The Motley Fool. All rights reserved.

Market data powered by Xignite and Polygon.io.