This Semiconductor Stock Has Jumped 48% in 2024, and Artificial Intelligence (AI) Could Help It Soar Further – The Motley Fool

Founded in 1993, The Motley Fool is a financial services company dedicated to making the world smarter, happier, and richer. The Motley Fool reaches millions of people every month through our premium investing solutions, free guidance and market analysis on Fool.com, top-rated podcasts, and non-profit The Motley Fool Foundation.

Founded in 1993, The Motley Fool is a financial services company dedicated to making the world smarter, happier, and richer. The Motley Fool reaches millions of people every month through our premium investing solutions, free guidance and market analysis on Fool.com, top-rated podcasts, and non-profit The Motley Fool Foundation.

You’re reading a free article with opinions that may differ from The Motley Fool’s Premium Investing Services. Become a Motley Fool member today to get instant access to our top analyst recommendations, in-depth research, investing resources, and more. Learn More

A turnaround in the fortunes of its largest customer could help this chipmaker deliver more upside.

Share prices of Cirrus Logic (CRUS 0.95%) have been in fine form so far in 2024, clocking gains of 48% as Wall Street turns bullish on the chipmaker’s prospects. The market is excited about a turnaround in the smartphone market, its solid quarterly results, and a potential improvement in the fortunes of its largest customer — Apple (AAPL -0.13%).

After all, Cirrus is highly reliant on Apple for a major chunk of its top line. In the recently concluded fiscal 2024 (which ended on March 30), Apple accounted for a whopping 87% of Cirrus’ revenue. Apple’s share of Cirrus’ top line has increased in recent years. Apple contracts accounted for 83% and 79% of its revenue in the preceding two fiscal years.

While reliance on a single customer for so much business is not a good thing, a turnaround in Apple’s fortunes related to its efforts in artificial intelligence (AI) could be a blessing in disguise for Cirrus Logic. Here’s why.

Cirrus Logic is known for supplying audio codecs, camera controllers, fast-charging chips, and haptics solutions to smartphone customers like Apple. It posted $372 million in revenue in the fourth quarter of fiscal 2024, which was flat on a year-over-year basis but crushed the Wall Street estimate of $317 million. The company’s non-GAAP (adjusted) earnings shot up an impressive 35% year over year to $1.24 per share, and the figure was nearly double the $0.64 per share consensus estimate.

Additionally, Cirrus’ forecast of $320 million in revenue in the current quarter at the midpoint of its guidance range added to investors’ bullishness as it was better than the $302 million analyst estimate. The guidance points toward a small jump in the top line from the prior-year period’s figure of $317 million.

So Cirrus’ fortunes are closely tied to Apple. This explains why Cirrus’ top-line growth wasn’t solid last quarter. Apple’s iPhone shipments, for instance, fell almost 10% year over year in the first quarter of calendar 2024, according to market research firm IDC. Sales of iPads and wearables also dropped. As a result, Apple’s overall revenue was down 4% year over year in the second quarter of fiscal 2024 (which ended on March 30).

The good news for Cirrus Logic is that Apple’s iPhone sales are expected to pick up pace as the year progresses, thanks to the proliferation of AI. Market research firm Counterpoint Research estimates that the AI smartphone market could clock a compound annual growth rate (CAGR) of 65% through 2027.

Though Apple doesn’t have an AI-capable phone in its portfolio yet (unlike Samsung), the company recently announced a slew of AI-related features that are expected to make their way to the next iPhone, which will go on sale later this year. From allowing users to leverage AI to summarize text to creating original images to transcribing phone calls, Apple has unveiled multiple features that could help it jump onto the AI bandwagon.

JPMorgan analyst Samik Chatterjee believes that the integration of AI-specific features in the 2024 iPhone models is likely to spur a solid upgrade cycle and help Apple sell more smartphones. More specifically, Chatterjee expects Apple to sell 244 million iPhone units in fiscal 2025, which would be a 10% increase from the estimated shipments in the current fiscal year. The momentum is expected to continue in fiscal 2026, with estimated shipments of 268 million units.

Moreover, as the tech giant’s Apple Intelligence platform is compatible only with the iPhone 15 Pro series and iPads and MacBooks powered by M1 chips, the company could witness the arrival of a solid device upgrade cycle. JPMorgan estimates that this new upgrade cycle will be equal to what Apple witnessed when 5G smartphones arrived, and it is worth noting that the tech specialist’s growth took off at that time.

Additionally, Apple is expected to release MacBooks with AI-capable chips this year, which would allow the company to tap another potentially lucrative market. All this bodes well for Cirrus Logic and explains why analysts have been turning bullish about its prospects.

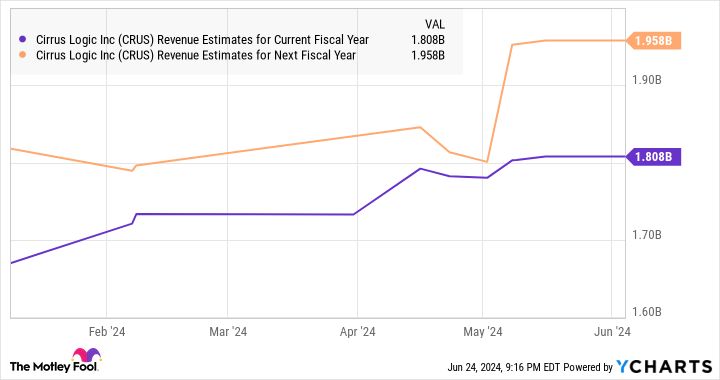

Cirrus Logic’s revenue in fiscal 2024 was down almost 6% from the previous year to $1.79 billion. However, analysts are expecting it to report a small improvement in the current fiscal year, which is evident from the following chart.

CRUS Revenue Estimates for Current Fiscal Year data by YCharts

As the chart above indicates, analysts increased their revenue guidance for the next fiscal year and expect Cirrus to deliver stronger growth. The prospects of AI-enabled smartphones and PCs and Cirrus’ relationship with a top player such as Apple in these markets should help it sustain healthy growth for a long time to come.

That’s why investors would do well to buy Cirrus Logic stock while it is still cheap. This semiconductor stock trades at 26 times trailing earnings right now, a discount to the Nasdaq-100‘s trailing earnings multiple of 32 (using the index as a proxy for tech stocks). We saw that Cirrus’ earnings accelerated nicely in the previous quarter, and the company could sustain that trend with Apple’s help.

As such, there is a good chance that Cirrus may be able to add to the already impressive gains it clocked in 2024.

Harsh Chauhan has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Apple. The Motley Fool recommends Cirrus Logic. The Motley Fool has a disclosure policy.

Invest better with The Motley Fool. Get stock recommendations, portfolio guidance, and more from The Motley Fool’s premium services.

Making the world smarter, happier, and richer.

© 1995 – 2024 The Motley Fool. All rights reserved.

Market data powered by Xignite and Polygon.io.