Missed Out on Nvidia? Buy ASML Stock Instead – The Motley Fool

Founded in 1993, The Motley Fool is a financial services company dedicated to making the world smarter, happier, and richer. The Motley Fool reaches millions of people every month through our premium investing solutions, free guidance and market analysis on Fool.com, top-rated podcasts, and non-profit The Motley Fool Foundation.

Founded in 1993, The Motley Fool is a financial services company dedicated to making the world smarter, happier, and richer. The Motley Fool reaches millions of people every month through our premium investing solutions, free guidance and market analysis on Fool.com, top-rated podcasts, and non-profit The Motley Fool Foundation.

You’re reading a free article with opinions that may differ from The Motley Fool’s Premium Investing Services. Become a Motley Fool member today to get instant access to our top analyst recommendations, in-depth research, investing resources, and more. Learn More

The semiconductor equipment manufacturer holds the key to this fast-growing industry.

Nvidia (NVDA 0.64%) stock’s artificial intelligence (AI)-powered surge has sent its valuation to incredible levels, putting the chipmaker well out of reach of value investors looking to capitalize on the proliferation of this technology.

Nvidia’s sales multiple of 36 and trailing earnings multiple of 73 are significantly higher than the technology sector’s price-to-sales ratio of 7.2 and earnings multiple of 45. Of course, Nvidia’s forward price-to-earnings ratio of 35 indicates that the semiconductor bellwether is on track to deliver terrific growth and could justify its expensive valuation.

But there is also a relatively inexpensive way for investors to ride the AI boom. Dutch semiconductor equipment company ASML (ASML -1.51%) is not only cheaper than Nvidia, but it is also playing a critical role in the growth of AI. Let’s look at the reasons why investors who have missed Nvidia’s stunning rally over the past year would do well to buy ASML right now.

There is no doubt that Nvidia’s graphics processing units (GPUs) play a central role in training large language models, but making those GPUs wouldn’t have been possible without ASML’s machines. More specifically, Nvidia’s flagship H100 AI GPU is manufactured using a custom 5-nanometer process node from Taiwan Semiconductor Manufacturing, popularly known as TSMC.

However, TSMC can only manufacture these 5nm chips using ASML’s machines. As it turns out, any semiconductor foundry that’s looking to manufacture advanced chips made on process nodes that are 7nm or smaller will have to turn to ASML’s extreme ultraviolet (EUV) lithography machines. That’s because ASML has a monopoly on the market for EUV lithography machines.

This puts the company in a solid position to make the most of the increasing demand for the advanced chipmaking equipment that will be needed to manufacture AI chips. According to third-party estimates, the EUV lithography market could clock a compound annual growth rate (CAGR) of 22% through 2032, generating $63 billion in annual revenue at the end of the forecast period. The overall semiconductor equipment market, meanwhile, is expected to generate a whopping $222 billion in revenue in 2032, up from $83 billion in 2022.

ASML’s massive order backlog makes it clear that it is well on its way to making the most of this multibillion-dollar opportunity. The company finished 2023 with a backlog of 39 billion euros. This impressive backlog was driven by a sharp jump in ASML’s bookings last quarter. More specifically, ASML recorded net bookings of 9.2 billion euros in the fourth quarter of 2023, a big jump over the 2.6 billion euros worth of bookings it received in the third quarter.

The company saw a sharp jump in orders last year, with its net bookings increasing by more than 50% to 30.7 billion euros from 20 billion euros in 2022. It is worth noting that 60% of the orders ASML received in the previous quarter were for EUV systems. That wasn’t surprising, as chipmakers are scrambling to place orders for ASML’s systems so that they can manufacture AI chips.

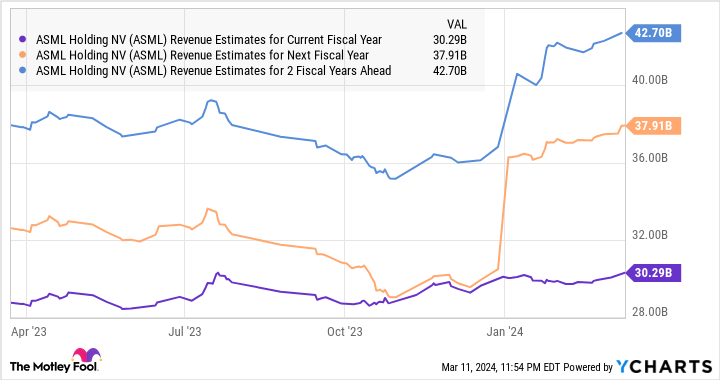

The company’s robust order backlog is the reason why it is predicted to deliver robust growth over the next couple of years.

ASML Revenue Estimates for Current Fiscal Year data by YCharts

ASML’s healthy top-line growth explains why its earnings are predicted to increase at an annual rate of 22% for the next five years. Based on its 2023 earnings of $21.78 per share, ASML’s bottom line could jump to just under $59 per share in 2028.

Using the Nasdaq-100‘s forward earnings multiple of 31 as a proxy for tech stocks and multiplying it by ASML’s projected earnings after five years points toward a stock price of $1,829. That would be a 90% increase from current levels. ASML currently trades at 46 times trailing earnings and 13 times sales, so it is significantly cheaper than Nvidia. This makes ASML an ideal bet for investors looking for a cheaper AI alternative to Nvidia, and they would do well to buy it before it soars further following 27% gains in 2024.

Harsh Chauhan has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends ASML, Nvidia, and Taiwan Semiconductor Manufacturing. The Motley Fool has a disclosure policy.

Invest better with The Motley Fool. Get stock recommendations, portfolio guidance, and more from The Motley Fool’s premium services.

Making the world smarter, happier, and richer.

© 1995 – 2024 The Motley Fool. All rights reserved.

Market data powered by Xignite and Polygon.io.