Is It Too Late to Buy Nvidia Stock After Its 10-for-1 Split? – The Motley Fool

Founded in 1993, The Motley Fool is a financial services company dedicated to making the world smarter, happier, and richer. The Motley Fool reaches millions of people every month through our premium investing solutions, free guidance and market analysis on Fool.com, top-rated podcasts, and non-profit The Motley Fool Foundation.

Founded in 1993, The Motley Fool is a financial services company dedicated to making the world smarter, happier, and richer. The Motley Fool reaches millions of people every month through our premium investing solutions, free guidance and market analysis on Fool.com, top-rated podcasts, and non-profit The Motley Fool Foundation.

You’re reading a free article with opinions that may differ from The Motley Fool’s Premium Investing Services. Become a Motley Fool member today to get instant access to our top analyst recommendations, in-depth research, investing resources, and more. Learn More

Nvidia stock is up nearly 800% over the last 18 months.

Artificial intelligence (AI) is one of the hottest industries for investors right now. Semiconductor darling and data center specialist Nvidia (NVDA 1.44%) is considered by many on Wall Street to be a lucrative opportunity for AI enthusiasts.

With shares of Nvidia up over 170% so far in 2024, some investors may think they’ve missed the boat.

Let’s take a look at what is going on at Nvidia, and assess if now is still a reasonable time to scoop up some shares.

2023 marked a new age for the technology industry. Behemoths such as Microsoft, Alphabet, and Amazon all made a series of splashy investments revolving around AI applications.

Some of the bigger investments these tech giants made were buying AI-powered semiconductor chips, as well as ramping up data center services. Considering Nvidia has an estimated 80% share of the AI chip market, these moves by big tech undoubtedly served as a big boost to the company.

The strong momentum from last year’s AI euphoria carried into 2024, and Nvidia investors haven’t stopped buying up the stock. To put this into context, shares of Nvidia have increased almost 800% since January 2023.

This unprecedented run briefly catapulted Nvidia over Microsoft as the world’s most valuable company by market cap. Moreover, as shares continued to eclipse new heights, Nvidia’s management finally decided to implement a 10-for-1 stock split last month.

Image source: Getty Images.

What’s incredible is that much of the narrative surrounding Nvidia deals with the company’s chip business. Indeed, its H100 and A100 graphics processing units (GPUs) are used by companies all around the world — including Meta Platforms and Tesla.

Moreover, Nvidia is continuing to lead the innovation front in the GPU realm with the introduction of its new Blackwell and Rubin chips.

With that said, it’s important to understand that Nvidia makes money from other products and services as well. In fact, one of its lesser-known growth opportunities is outside of hardware.

Nvidia’s compute unified device architecture (CUDA) software platform is already proving to be a lucrative business. Essentially, CUDA is a programming tool that is meant to be used in parallel with Nvidia’s GPUs. So, in a sense, the company is attempting to build out an end-to-end AI ecosystem encompassing both hardware and software.

One of the big reasons CUDA is going to be important for Nvidia is due to competition in the chip space. Companies such as AMD, Intel, and even Amazon and Meta are all working on competing GPUs to that of Nvidia.

Although it’s too early to get a sense of how these competing products will impact Nvidia, I think it’s reasonably safe to say that the company will eventually lose some of its pricing power in the chip space. As a result, Nvidia’s profit margins are likely to take a hit at some point in the future. However, some of this margin deterioration should be mitigated so long as CUDA continues to thrive. The reason is because software products tend to carry much higher margins than hardware.

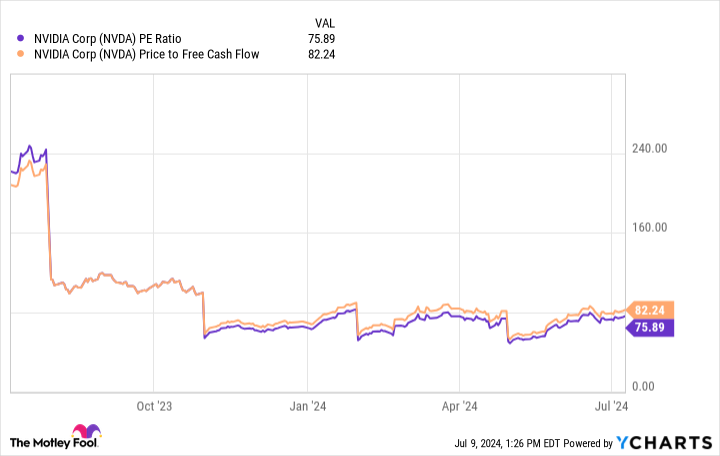

The chart below illustrates Nvidia’s price-to-earnings (P/E) and price-to-free-cash-flow (P/FCF) multiples over the last 12 months. While a P/E of 75.9 and a P/FCF of 82.2 may look pricey, there are a couple of ideas to explore here.

NVDA PE Ratio data by YCharts

First, both Nvidia’s P/E and P/FCF multiples are lower than they were a year ago. In other words, despite the rapid ascent of the stock price, Nvidia’s earnings and cash flow are accelerating at a faster rate — therefore, Nvidia stock is technically less expensive today than it was 12 months ago.

Moreover, Nvidia’s commanding lead in the chip space and its under-the-radar software services should be analyzed further. The company is an investor in Databricks, one of the most valuable AI start-ups in the world. Nvidia is also an investor in Figure AI — a developer of humanoid robotics.

I do not think that opportunities in robotics and AI software are priced into Nvidia stock yet. I think many of these applications are currently overshadowed by the performance of the chip business, and many investors are discounting the potential Nvidia has in other areas in the AI arena.

Long-term investors have an opportunity to gain exposure to many different aspects of AI simply through Nvidia. Despite the meteoric rise in share price, the valuation analysis above, as well as some of the other growth opportunities explored make a compelling case that Nvidia stock is a good buy right now and significant upside could very much be in store.

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Randi Zuckerberg, a former director of market development and spokeswoman for Facebook and sister to Meta Platforms CEO Mark Zuckerberg, is a member of The Motley Fool’s board of directors. Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool’s board of directors. Adam Spatacco has positions in Alphabet, Amazon, Meta Platforms, Microsoft, Nvidia, and Tesla. The Motley Fool has positions in and recommends Advanced Micro Devices, Alphabet, Amazon, Meta Platforms, Microsoft, Nvidia, and Tesla. The Motley Fool recommends Intel and recommends the following options: long January 2025 $45 calls on Intel, long January 2026 $395 calls on Microsoft, short August 2024 $35 calls on Intel, and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

Invest better with The Motley Fool. Get stock recommendations, portfolio guidance, and more from The Motley Fool’s premium services.

Making the world smarter, happier, and richer.

© 1995 – 2024 The Motley Fool. All rights reserved.

Market data powered by Xignite and Polygon.io.