Is ASML Stock a Buy Now? – The Motley Fool

Founded in 1993, The Motley Fool is a financial services company dedicated to making the world smarter, happier, and richer. The Motley Fool reaches millions of people every month through our premium investing solutions, free guidance and market analysis on Fool.com, top-rated podcasts, and non-profit The Motley Fool Foundation.

Founded in 1993, The Motley Fool is a financial services company dedicated to making the world smarter, happier, and richer. The Motley Fool reaches millions of people every month through our premium investing solutions, free guidance and market analysis on Fool.com, top-rated podcasts, and non-profit The Motley Fool Foundation.

You’re reading a free article with opinions that may differ from The Motley Fool’s Premium Investing Services. Become a Motley Fool member today to get instant access to our top analyst recommendations, in-depth research, investing resources, and more. Learn More

Should investors buy this semiconductor giant following its recent dip?

Semiconductor giant ASML (ASML -1.51%) has lost its spark recently after a solid start to 2023, with shares of the company now up just 10% year to date despite the impressive growth that it’s delivering quarter after quarter.

As it turns out, ASML stock is down 12% in the past three months. Even worse, it looks like the stock will remain under pressure following its third-quarter 2023 results (released on Oct. 18). Investors were quick to press the panic button after seeing what ASML reported. Let’s see why that was the case and check if the stock’s recent slip could be a buying opportunity for savvy investors.

ASML’s Q3 revenue increased 16% year over year to 6.7 billion euros. Its adjusted net income increased to 4.81 euros per share from 4.29 euros per share in the prior-year period, a jump of 12%. In U.S. dollar terms, the Dutch semiconductor equipment supplier delivered $5.23 per share in earnings on $7.26 billion in revenue. Analysts predicted earnings of $4.92 per share on revenue of $7.19 billion. What’s more, ASML reiterated its 2023 revenue growth forecast of 30%, indicating that its annual revenue is on track to jump to 27.5 billion euros from last year’s level of 21.2 billion euros.

All those results sound solid. So why are investors panicking? The company’s 2024 guidance got alarm bells ringing as ASML anticipates no growth in revenue next year.

Management says the semiconductor industry is “currently working through the bottom of the cycle and our customers expect the inflection point to be visible by the end of this year. Customers continue to be uncertain about the shape of the demand recovery in the industry.” This customer uncertainty is reflected in the orders for ASML’s lithography machines that play a critical role in the manufacturing of semiconductors that are deployed across multiple applications, including artificial intelligence (AI).

More specifically, ASML received net bookings worth 2.6 billion euros for its machines last quarter. This metric refers to the sales orders for ASML’s systems for which the company has received written authorizations. The net bookings figure fell from the Q2 reading of 4.5 billion euros. The decline was even more alarming on a year-over-year basis as it received net bookings worth 8.9 billion euros in the third quarter of 2022.

The fact that ASML’s bookings were substantially lower than its sales is likely to put the company’s growth trajectory under pressure. However, there is a chance that ASML may turn in a better-than-expected performance next year before stepping on the gas in 2025.

Though ASML saw a sharp decline in bookings last quarter, the company is sitting on a solid backlog worth 35 billion euros. The semiconductor bellwether expects revenue of 6.9 billion euros in the current quarter. So, its backlog is strong enough to help it achieve its goal of flat revenue growth in 2024 even if no new orders come in (assuming it can convert its entire backlog into revenue).

What’s more, ASML expects 2025 to be “a significant growth year” thanks to the construction of new semiconductor fabrication plants. The company points out that the growing demand for chips from verticals such as AI and electric vehicles will require more capacity investments.

Data platform provider Z2Data points out that there are 73 semiconductor fabs under construction globally. Of these, 50 fabs are being built from scratch, while the remaining 23 are expansions of existing fabs. It is worth noting that 21 of these 50 new fabs are being built in the U.S. Z2Data estimates that 53 of these 73 total fabs are likely to be completed within the next four years.

Precedence Research estimates that the global semiconductor market could grow from an annual revenue of $592 billion in 2022 to $1.88 trillion in 2032, clocking a compound annual growth rate of 12%. This explains why new fabs are coming up around the world, and this should present a secular growth opportunity for ASML in the long run.

Not surprisingly, industry association SEMI estimates that spending on semiconductor manufacturing equipment could rebound from 2024. SEMI forecasts a 19% decline in semiconductor manufacturing equipment spending in 2023 to $87 billion before nearing $100 billion next year. As such, the possibility of ASML getting new bookings from next year should not be ruled out despite the cautious forecast it issued last week.

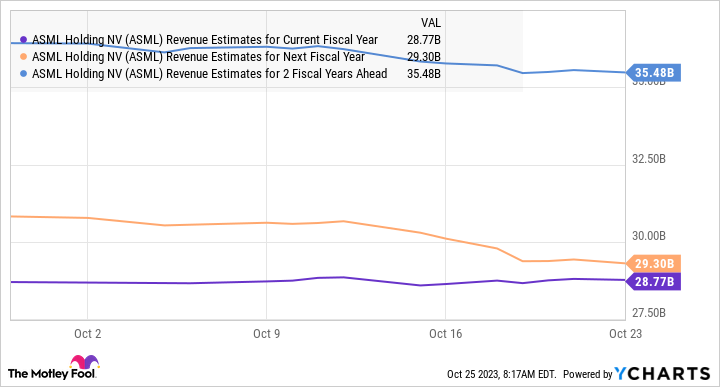

This explains why analysts anticipate a jump in ASML’s top line from 2025, and it should be able to sustain that momentum for a longer time as its five-year annual earnings growth forecast of 23% indicates.

ASML Revenue Estimates for Current Fiscal Year data by YCharts

All this indicates that investors would do well to take advantage of the slide in ASML to accumulate this semiconductor stock as it could regain its mojo and deliver solid long-term gains. After all, it is now trading at 29 times trailing earnings, a nice discount to its five-year average price-to-earnings ratio of 41.

If the stock continues to remain under pressure and becomes cheaper, buying it could be a no-brainer move from a long-term perspective as ASML’s dominant position in the semiconductor equipment market puts it in a solid position to capitalize on the secular growth opportunity in this space.

Harsh Chauhan has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends ASML. The Motley Fool has a disclosure policy.

Invest better with The Motley Fool. Get stock recommendations, portfolio guidance, and more from The Motley Fool’s premium services.

Making the world smarter, happier, and richer.

© 1995 – 2024 The Motley Fool. All rights reserved.

Market data powered by Xignite and Polygon.io.