Doanh thu của ngành đúc toàn cầu tăng nhờ nhu cầu về AI

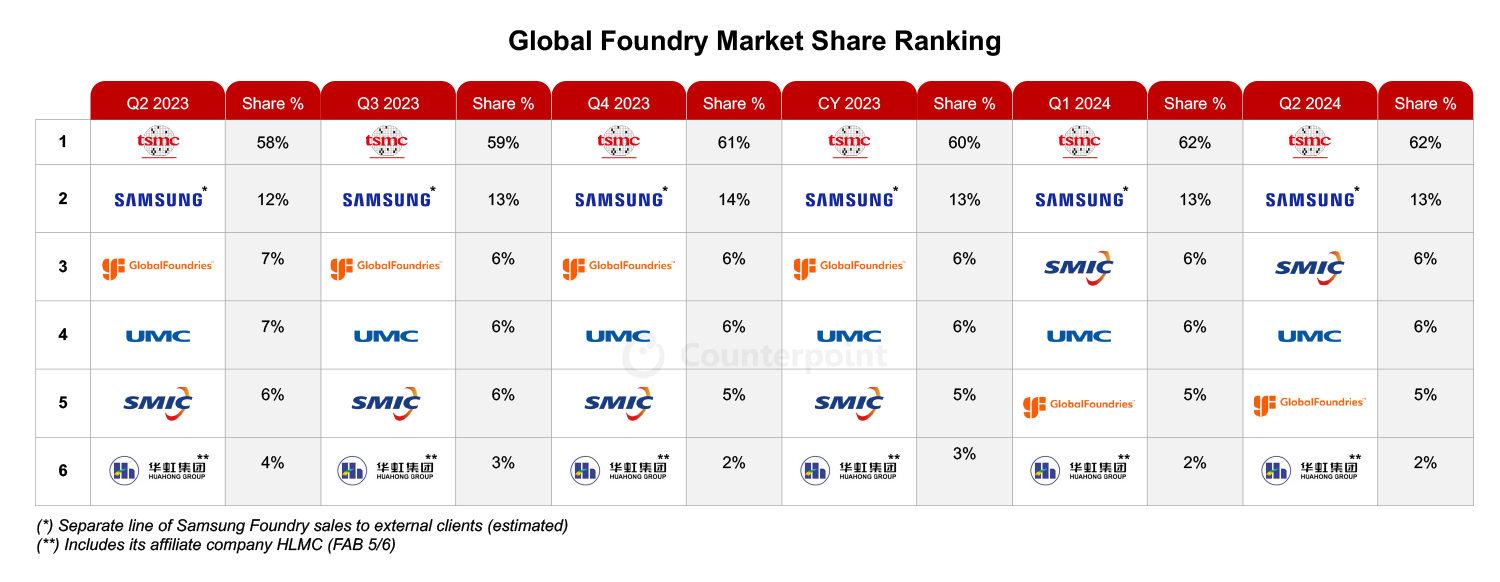

The global foundry industry’s revenue grew about 9% QoQ and 23% YoY in Q2 2024, according to Counterpoint Research’s Foundry Quarterly Tracker. The sequential growth was mainly driven by strong AI demand. CoWoS supply remained tight, with potential upsides in capacity expansions focusing on CoWoS-L going forward. Despite slower demand recovery for non-AI semiconductors, such as those used in automotive and industrial applications, we observed some rush orders for certain applications, such as IoT and consumer electronics. Notably, China’s foundry and semiconductor market saw a faster recovery compared to global peers. Chinese foundry players such as SMIC and HuaHong delivered strong quarterly results and positive guidance, as China’s fabless customers entered the inventory correction phase earlier, bottoming out sooner than their global counterparts.

Source: Counterpoint Research

TSMC delivered a mild quarterly revenue beat in Q2 2024, driven by continuing strong growth in AI accelerator demand. As a result, TSMC further revised its annual revenue guidance to mid-20% from low-to-mid 20% earlier. Besides, TSMC expects the demand-supply balance for AI accelerators to remain tight through late 2025 or early 2026. The company also plans to at least double its CoWoS capacity again in 2025 to meet strong AI demand from customers. Also, we continue to believe that potential price hikes for advanced nodes, such as 3nm and 5/4nm, are highly likely in 2025, underscoring TSMC’s technology leadership and boding well for the company’s long-term profitability and the industry’s sustained growth.

Samsung Foundry’s revenue increased sequentially primarily due to inventory pre-build and restocking for smartphones, maintaining its second position with a 13% market share in Q2 2024. The company continues to focus on securing more mobile and AI/HPC customers for advanced nodes and expects its annual revenue growth to outpace industry growth.

SMIC’s quarterly results were strong, and the company provided stronger-than-expected guidance for Q3, driven by continued demand recovery in China, including for CIS, PMIC, IoT, TDDI and LDDIC applications. SMIC’s 12” demand is improving, and blended ASP (average selling price) is expected to increase as inventory restocking broadens among Chinese fabless customers. The company is cautiously optimistic about its annual revenue growth, with a healthy utilization uptick expected going forward.

UMC reported a strong beat in its quarterly results largely due to a better margin profile, thanks to favorable foreign exchange rates and disciplined pricing power. The company guided mid-single-digit sequential growth for Q3 2024, in line with our forecast as we observe a weaker recovery in overall logic semiconductors except for AI. UMC’s strategy to focus on specialized technologies such as 22nm HV and 55nm RF SOI/BCD, and reduced exposure to commoditized areas such as LDDIC and NOR flash, is expected to support stable pricing and long-term growth.

GlobalFoundries’ quarterly results were solid. Driven by the ramp-up of new design wins, the company’s automotive business grew sequentially despite a challenging market. The company is also seeing normalizing inventories in the smartphone market and stabilizing demand in the communication and IoT markets. GlobalFoundries’ guidance indicates a mild recovery in its overall business, echoing trends seen in other non-Chinese mature node foundries such as UMC.

Counterpoint Research Analyst Adam Chang said, “In Q2 2024, the global foundry industry demonstrated resilience, with most of the growth primarily driven by robust AI demand and smartphone inventory restocking. Demand recovery across the semiconductor industry is progressing unevenly. While leading-edge applications such as AI semiconductors are experiencing strong growth, traditional semiconductors are recovering more slowly. Chinese foundries are rebounding faster due to earlier inventory corrections and increased restocking by local fabless customers. In contrast, non-Chinese foundries are experiencing a more gradual recovery.”

Background

Counterpoint Technology Market Research is a global research firm specializing in products in the TMT (technology, media and telecom) industry. It services major technology and financial firms with a mix of monthly reports, customized projects and detailed analyses of the mobile and technology markets. Its key analysts are seasoned experts in the high-tech industry

Contact information: