Better Artificial Intelligence Stock: TSMC vs. ASML Holding – The Motley Fool

Founded in 1993, The Motley Fool is a financial services company dedicated to making the world smarter, happier, and richer. The Motley Fool reaches millions of people every month through our premium investing solutions, free guidance and market analysis on Fool.com, top-rated podcasts, and non-profit The Motley Fool Foundation.

Founded in 1993, The Motley Fool is a financial services company dedicated to making the world smarter, happier, and richer. The Motley Fool reaches millions of people every month through our premium investing solutions, free guidance and market analysis on Fool.com, top-rated podcasts, and non-profit The Motley Fool Foundation.

You’re reading a free article with opinions that may differ from The Motley Fool’s Premium Investing Services. Become a Motley Fool member today to get instant access to our top analyst recommendations, in-depth research, investing resources, and more. Learn More

Both semiconductor titans are on track to capitalize on the AI boom, but which one should you be putting your money on right now?

The PHLX Semiconductor Sector index has been in rip-roaring form on the market over the past year, clocking outstanding gains of 60% as of this writing and handsomely outpacing the 28% gains that the S&P 500 index has delivered during the same period.

Artificial intelligence (AI) has played a central role in this terrific surge as demand for chips required in training and inferencing of AI models has surged remarkably. As a result, key industry players such as Taiwan Semiconductor Manufacturing (TSM -1.13%) and ASML Holding (ASML -1.62%) have benefited mightily. Shares of Taiwan Semiconductor, better known as TSMC, have soared 85% in the past year, while ASML is sitting on gains of 53%.

Both companies are playing a central role in the AI chip market. However, if you had to choose just one of these two semiconductor stocks to capitalize on the AI boom, which one should you buy? Let’s find out.

TSMC is the world’s largest semiconductor foundry with a market share of 62% in the first quarter of 2024. It is ahead of the second-largest foundry Samsung, which has a market share of 13%, by a huge margin. TSMC’s terrific lead in the foundry market means that it is the go-to choice for fabless chipmakers (who only design their chips but outsource the manufacturing to foundry partners such as TSMC) looking to make the most of the terrific demand for AI chips.

What’s more, TSMC’s foundry market share has increased on the back of AI-driven demand. Its market share increased by three percentage points on a year-over-year basis inQ1. Allied Market Research estimates that the semiconductor foundry market could generate annual revenue of more than $231 billion in 2032, more than double the $106 billion it generated in 2022.

There is a good chance that TSMC could continue to grab a bigger share of this lucrative market and continue to pull ahead of its rivals thanks to its advanced chip manufacturing processes that are powering AI applications. It is worth noting that top chipmakers such as Nvidia, Intel, and AMD have been using TSMC’s foundries to manufacture AI chips.

Nvidia’s popular H100 AI chip, for instance, is based on TSMC’s manufacturing node, and the graphics card specialist is tapping the latter for its new Blackwell chips as well. Similarly, AMD’s latest AI chips are based on TSMC’s manufacturing node, and the chipmaker also plans to continue collaborating with the foundry giant for future chips.

TSMC’s strong clientele in AI chips bodes well for its future, as demand for AI chips is forecast to increase at a compound annual growth rate of nearly 30% through 2032, outpacing the growth of the foundry market noted above. As a result, there is a good chance that TSMC could outgrow the industry in which it operates.

The good part is that AI-driven demand has led to an acceleration in TSMC’s growth this year. Its revenue in the first five months of the year has increased by 27% from the same period last year. Analysts are forecasting TSMC’s revenue to grow 23% in 2024 to $85 billion, but its current pace of growth suggests that it could do even better.

Throw in additional catalysts in the smartphone and personal computer (PC) markets, where AI is expected to drive stronger sales growth, and it is easy to see why analysts have substantially increased their growth expectations from TSMC of late. The company’s 2024 earnings estimate has risen from $5.76 per share three months ago to $6.35 per share now, a trend that could continue based on the discussion above.

TSMC, therefore, could continue to be a top beneficiary of the growing adoption of AI and continue to rally higher.

The advanced AI chips that TSMC manufactures for its clients wouldn’t be possible without ASML’s machines. The Dutch semiconductor equipment giant’s monopoly in the extreme ultraviolet (EUV) lithography space means that chipmakers and foundries such as TSMC need to rely on ASML’s offerings to make chips that are both powerful and power-efficient at the same time.

After all, manufacturing chips on 7-nanometer (nm), 5nm, and 3nm nodes, which are used for AI applications, is possible only with ASML’s machines. This explains why demand for its machines has been robust in recent years, allowing the company to build a solid backlog of orders that should allow it to deliver healthy long-term growth.

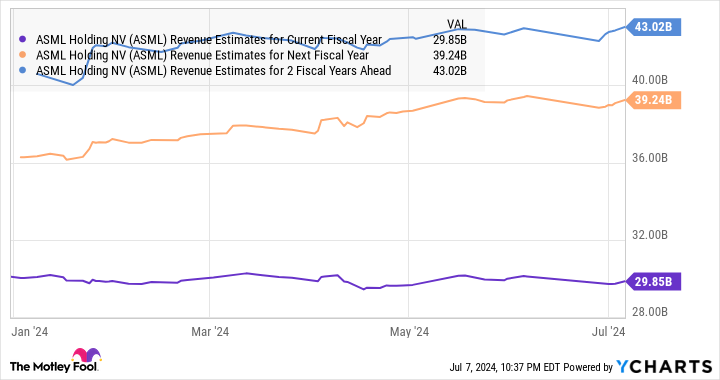

More specifically, ASML was sitting on an order backlog worth 38 billion euros at the end of the first quarter of 2024. That’s higher than the company’s full-year revenue forecast of 27.5 billion euros, which is in line with its 2023 sales. It is worth noting that ASML could convert more of its backlog into revenue in 2024 as it has begun shipments of its advanced chipmaking machine that reportedly costs $380 million per unit.

More importantly, ASML is looking to increase the manufacturing capacity of its advanced machinery over the next few years. That’s not surprising, as its customers such as TSMC are looking to make chips on even smaller process nodes to tackle AI-related workloads. For example, TSMC believes that its 3nm process node could create $1.5 trillion worth of products during a five-year period.

As a result, there is a good chance that ASML will continue to witness an increase in its order book as its customers buy more of its machines to make more efficient chips. Not surprisingly, the company’s top line is expected to jump substantially in 2025 following this year’s flat performance, which is a hangover of last year’s weak semiconductor demand as its customers continue to work through existing inventory levels.

ASML Revenue Estimates for Current Fiscal Year data by YCharts

As such, even ASML could turn out to be a top AI stock in the future and deliver stronger gains than it has clocked in the past year. But is it a better buy than TSMC?

If we take a closer look at the valuation of these two companies, it will be evident that TSMC is the more affordable of the two right now. TSMC’s trailing price-to-earnings (P/E) ratio stands at 34, which is significantly cheaper than ASML’s multiple of almost 55. Moreover, TSMC has a forward P/E ratio of 29, which is again much lower than ASML’s multiple of 51.

Given that TSMC is growing at a faster pace than ASML and the shares are trading at a much more attractive valuation, it looks like the better AI stock to buy of the two. However, it would be wise to keep a close watch on ASML as well, as an acceleration in its growth thanks to its massive backlog could send its shares soaring in the long run.

Harsh Chauhan has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends ASML, Advanced Micro Devices, Nvidia, and Taiwan Semiconductor Manufacturing. The Motley Fool recommends Intel and recommends the following options: long January 2025 $45 calls on Intel and short August 2024 $35 calls on Intel. The Motley Fool has a disclosure policy.

Invest better with The Motley Fool. Get stock recommendations, portfolio guidance, and more from The Motley Fool’s premium services.

Making the world smarter, happier, and richer.

© 1995 – 2024 The Motley Fool. All rights reserved.

Market data powered by Xignite and Polygon.io.