Navitas Semiconductor: Setting Up For 2025 (NASDAQ:NVTS) – Seeking Alpha

bombermoon

bombermoon

Navitas Semiconductor (NASDAQ:NVTS) reported earnings in May, and the market sold off the stock.

In this earnings review, I will share more about my views about the 1Q24 report.

I have covered Navitas Semiconductor extensively on Seeking Alpha, which can be found here, and I continue to be positive about the company’s improving fundamentals despite some near-term moderation in growth in some segments.

In the 1Q24 earnings result, management’s forward-looking commentary for the remainder of 2024 was worse than one quarter ago.

Management commented that they have not yet seen signs of a broader market recovery for the second half of 2024:

Overall, we have not yet observed any signs of a broader market recovery in the second half of the year, and this may translate to a more moderated growth in 2024.

In 2Q24, Navitas Semiconductor continues to see softness.

Although it is said that there is a chance that 2Q24 could be the bottom, the company does not have strong visibility on the 3Q24 quarter.

As a result, it does seem management is less confident that it is able to achieve the 40% to 50% revenue growth guidance for 2024, thereby calling for a more moderated growth in 2024.

For the 2Q24 guidance, management expects revenues of $20 million at the midpoint, which is just a 10% growth from the prior year and down sequentially from 1Q24.

This soft guidance is a result of lower demand for its EV, solar and industrial markets.

That said, its customer pipeline continues to grow, with many new production programs starting or ramping in 2025.

The customer pipeline of $1.25 billion as of December 2023 grew by 28% to $1.6 billion as of the end of 1Q24.

This illustrates the strong future growth for Navitas Semiconductor outside of 2024, as much of that pipeline growth will only contribute to revenues in 2025.

Firstly, within the data center segment, the company expects multiple millions in revenue in 2024 and between $10 million to $20 million in 2025.

Navitas Semiconductor announced that it has won three major design wins with the largest power supply companies in the world.

With more than 30 customer projects currently in development, some of which include the big names like Amazon (AMZN), Microsoft (MSFT), Google (GOOG), Super Micro Computer (SMCI), we will see Navitas Semiconductor’s GaN products in many data centers in the near future.

The acceleration in demand from the data center segment is of course a result of the developments around AI.

Nvidia (NVDA) Blackwell chipset requires more than 1,000 watts, compared to traditional data center processors which require just 300 watts to 400 watts.

The transition from traditional data center processors to Nvidia’s Blackwell chipsets means that there is a 300% increase in power requirements in only 18 months, along with a 96% minimum energy efficiency standard to be met.

Navitas Semiconductor is able to increase server power from 3.2 kilowatts at 96% efficiency to 8 to 10 kilowatts at 97% efficiency as a result of its leading-edge GaNSafe technology, along with the industry-leading Gen-3 Fast silicon carbide and the company’s unique data center system design capability. This new data center product is expected to be delivered to customers later in 2024.

Secondly, the EV pipeline increased by more than 50%, from the $400 million announced last December.

There is a significant expansion in Navitas Semiconductor customer pipeline as a result of interest from not just passenger battery EVs, plug-in hybrids, commercial EVs and even fuel cell hydrogen clean energy cars.

The current 6.6-kilowatt onboard charger platform that was designed by the EV system design team is driving significant customer adoption.

In addition, a new 22-kilowatt onboard charger platform was recently launched, which brings three times faster charging and double the power density.

Both these onboard charger platforms should drive considerable new revenues in 2025, with new silicon carbide customer projects ramping in the first half of 2024, along with growing EV adoption.

Navitas Semiconductor now has more than 160 EV related customer projects across regions, which should bring tens of millions of revenues in 2025.

Thirdly, for the solar and energy storage segment, the customer pipeline has increased significantly from the earlier $250 million reported in December 2023.

There were six new wins for the segment across US, Europe, and Asia. Management is seeing signs of recovery, as these wins are spread across solar optimizers, micro-inverters, string inverters, and energy-storage applications.

These wins are expected to start ramping in 2025.

Navitas Semiconductor highlighted one major microinverter leader, which committed to a major transition to GaN in the first half of 2025, which will bring revenues worth tens of millions to Navitas Semiconductor.

Fourthly, the appliance and industrial customer pipeline has also grown significantly compared to the $360 million reported last December.

There was notable progress in 1Q24, where the latest motor-optimized GaNSense half-bridge now has over 15 customer projects in development.

These customers include a European leader in haircare, which will launch in late 2024, a tier 1 US-based dishwasher supplier, and two of the top European leaders in pumps and motors, all of which will ramp in 2025.

Within the industrial segment, the latest Gen-3 Fast silicon carbide and GaNSafe technology are resulting in rapid adoption, leading to more than 25 customer developments.

Finally, the mobile and consumer markets remained strong as all major mobile OEMs continue to adopt GaN and replace silicon in a growing number of their chargers.

This trend is the same whether we look at smartphones, tablets, or notebooks.

In 1Q24, Navitas Semiconductor brought 20 new fast chargers into production.

With that, the total released customer products are now at more than 450, and it includes all of the top 10 mobile OEMs across smartphone and notebooks.

Management shared that to achieve operating margin breakeven, revenues need to be between $50 million to $55 million quarterly.

The new CFO on board is committed to driving profitable growth and to improving working capital efficiencies and making process improvements.

The new CFO also continues to be very confident in the long-term financial model that the company laid out in the investor day.

As I have discussed in the investor day article, in the long-term, Navitas intends to grow 6x to 10x the market and deliver at least 50% gross margins and 20% operating margins.

Given that Navitas Semiconductor is still burning cash as it is not quite operating at scale yet, the current $130 million in cash on its balance sheet should last at least three to four years before it needs additional capital.

I embedded 10% dilution assumptions in there given the lack of profitability in the near-term.

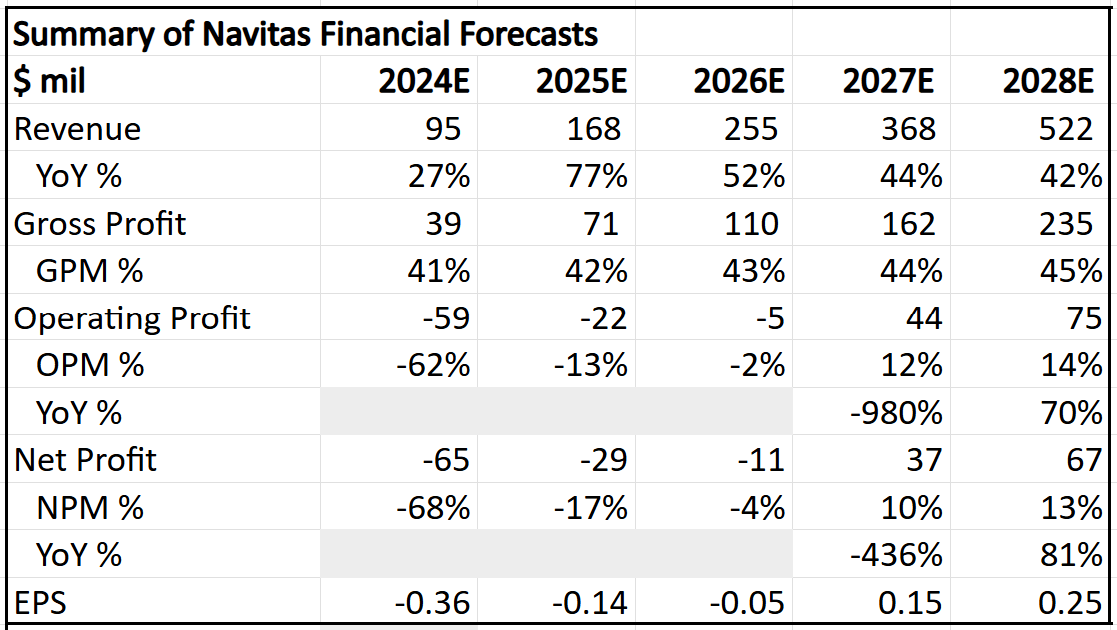

Also, I do think that there is a chance that my revenue forecasts are conservative, given that they are based on the building blocks of revenues based on each segment management has disclosed.

The margin assumptions are also kept conservative, given that I assume operating margins turn positive only at the revenue run rate of $368 million in 2027. I also assume that in 2028, gross margins and operating margins are at 45% and 14% respectively, nowhere near the long-term target margin levels.

Summary of 5-year financial forecasts (Author generated)

Summary of 5-year financial forecasts (Author generated)

While my terminal multiple and cost of equity remains at 40x and 15% respectively, the intrinsic value for Navitas Semiconductor goes down to $5.70 as a result of the slower growth in 2024 and higher dilution assumptions given the slower revenue ramp.

My 1-year and 3-year price targets are $4.70 and $8.30 respectively.

They imply 9x 2024 P/S and 6x 2026 P/S.

The takeaways in the 1Q24 were certainly not the best for the short-term investor, but for a long-term investor like me, I do not necessarily see this as thesis changing.

The expectation of a more moderate growth in the back half of 2024 is a result of continued challenges in some of the segments that were expected to contribute more significantly to growth this year.

This slower revenue growth in 2024 and uncertainty about how 2025 will look cause investors to sell off Navitas Semiconductor.

The reason is that the company is not yet profitable and needs to reach a revenue of $50 million each quarter to reach operating margin breakeven.

With the pushback in the recovery in the second half of 2024, this also implies that the profitability outlook becomes less certain.

In turn, this could mean greater dilution for shareholders if the company runs out of funds, although the company should have sufficient for the next three to four years based on the current cash on its balance sheet.

That said, I think that there are many other positive points, which includes the growth of the customer pipeline by 28% from December 2023, just a few months ago.

The positive contributions from data centers as a result of AI is also an interesting growth optionality and could accelerate in the medium to longer term.

Outperforming the Market is focused on helping you outperform the market while having downside protection during volatile markets by providing you with comprehensive deep dive analysis articles, the AI deep dive report, and access to The Barbell Portfolio.

The Barbell Portfolio outperformed the S&P 500 by 50% in the past year through owning high conviction growth and contrarian stocks.

Apart from providing bottom-up fundamental research, we also provide you with intrinsic value, 1-year and 3-year price targets in The Price Target report.

Join Outperforming the Market before the 20% price hike next month.

This article was written by

Analyst’s Disclosure: I/we have a beneficial long position in the shares of NVTS either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.