4 Threats to Nvidia Every Investor Needs to Know – The Motley Fool

Founded in 1993, The Motley Fool is a financial services company dedicated to making the world smarter, happier, and richer. The Motley Fool reaches millions of people every month through our premium investing solutions, free guidance and market analysis on Fool.com, top-rated podcasts, and non-profit The Motley Fool Foundation.

Founded in 1993, The Motley Fool is a financial services company dedicated to making the world smarter, happier, and richer. The Motley Fool reaches millions of people every month through our premium investing solutions, free guidance and market analysis on Fool.com, top-rated podcasts, and non-profit The Motley Fool Foundation.

You’re reading a free article with opinions that may differ from The Motley Fool’s Premium Investing Services. Become a Motley Fool member today to get instant access to our top analyst recommendations, in-depth research, investing resources, and more. Learn More

What could stand in the way of Nvidia's continued success?

The artificial intelligence (AI) gold rush is well underway and investors are looking for opportunities to strike it rich. The November 2022 launch of OpenAI’s ChatGPT for public use sparked the rush, helping push numerous stocks to new heights and contributing heavily to the S&P 500 index being up almost 42% over that timeframe. One of the biggest beneficiaries has been semiconductor specialist Nvidia (NVDA 1.44%). The chipmaker’s rise has been quite the story of the last few years; it’s up about 726% since ChatGPT’s launch. Over the past five years, it’s up nearly 3,000%.

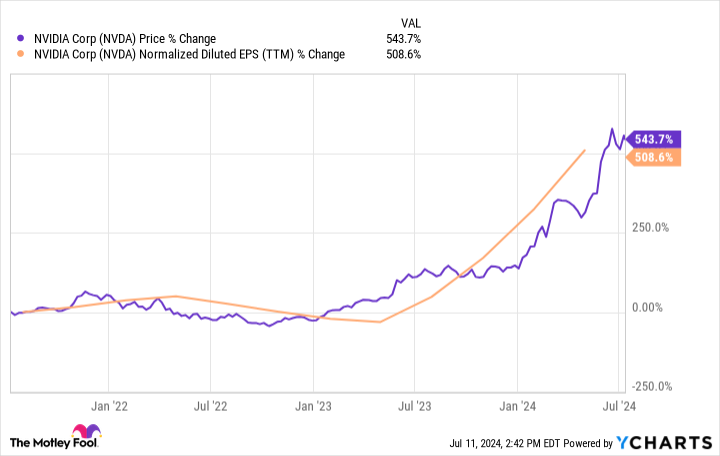

Nvidia keeps reporting massive earnings growth quarter after quarter, justifying an ever-higher stock price. The company is trading at a price-to-earnings ratio (P/E) only slightly higher than at the close of 2022. That’s impressive considering the outstanding stock price appreciation over that time. Take a look at the company’s earnings growth below compared to its share price over the past three years. Notice how the two keep pace with each other?

NVDA data by YCharts

Nvidia is keeping up with market expectations, at least thus far. Its dominance of the AI chip market and the vision it displayed to get there is impressive.

Past performance has been great, but investing is more about anticipating future performance and buying based on where you think the company is going. Investors should also consider what obstacles stand in the way of a company continuing to find success. Let’s take a look at four potential threats that could significantly impact Nvidia’s business (and its stock) in the future.

When you become one of the largest companies in the world in a relatively short time, you better expect competition to heat up. Nvidia proved that providing chips to the AI industry is a massively lucrative business, and others want in on the action. The most obvious competition comes from other chipmakers, most notably Advanced Micro Devices. The longtime rival of Nvidia has set its sights on taking market share. AMD CEO Lisa Su said at a recent unveiling of AMD’s latest chips that in no uncertain terms, “AI is our No. 1 priority.”

While this will put pressure on Nvidia, a bigger threat might actually involve the Big Tech clients currently fueling Nvidia’s massive revenue growth. A significant portion of Nvidia’s revenue is concentrated among firms like Meta Platforms, Microsoft, and Amazon. If that business dries up, it spells trouble for Nvidia’s bottom line.

Why would it dry up? The cost of AI chips is so great that some of these companies are working to design their own, in-house. This will take time, and success is far from guaranteed — it turns out that designing advanced microchips that can be built at scale is really hard — but any one of these companies, let alone several or all, replacing Nvidia chips with their own would likely be disastrous.

Without going into too much technical detail (which I’m in no way qualified to discuss) about the way AI algorithms function (especially large language models (LLMs) like ChatGPT), they seem to be suited perfectly to the kind of chip Nvidia designs, and they require a lot of them. This led to the massive demand that is driving Nvidia’s revenue.

However, technology can change, sometimes very quickly. A different kind of AI model could come into vogue that favors a different kind of chip or is significantly more efficient and needs fewer chips to function. A recent scientific paper proposes a new AI model that does just that, requiring only 10% of the chips used by current models. This would likely drive the demand for Nvidia’s chips down significantly and wreak havoc on the company’s bottom line.

Nvidia designs its chips and the software needed to operate them, but it shops out the production of those chips primarily through Taiwan Semiconductor Manufacturing, which is based in Taiwan. Although it’s unlikely to happen in the near future, the threat of China invading Taiwan should be taken seriously. If that happens, relations between China and the U.S. would be extremely fraught. Even if direct military conflict was avoided, it’s very possible that Nvidia’s operations in Taiwan would be shut down completely or boycotted by multiple countries. Relocating the manufacturing of Nvidia chips would be extremely costly for the company.

If AI turns out to be a bust, that is perhaps the biggest threat to the company. The promise of AI to revolutionize multiple sectors of the economy has been so hyped that most investors expect it is a foregone conclusion at this point. The sizeable amount of money flowing into the space is largely built on the promise of strong future returns.

Nvidia’s revenue over the past two years is real; I’m not disputing that. However, the demand for its chips will ultimately only be as strong as the demand for end-user AI technologies — technologies that deliver real economic value on par with the money being spent to develop and implement them. I am not saying this won’t happen, only that it wouldn’t be the first time a technology failed to deliver on the hype surrounding it (the hype around the metaverse is just the latest example of this).

It’s important to maintain a healthy skepticism in the midst of a run like Nvidia has had. Knowing this and knowing about the other potential threats will make you an informed Nvidia investor.

Randi Zuckerberg, a former director of market development and spokeswoman for Facebook and sister to Meta Platforms CEO Mark Zuckerberg, is a member of The Motley Fool’s board of directors. John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Johnny Rice has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Advanced Micro Devices, Amazon, Meta Platforms, Microsoft, Nvidia, and Taiwan Semiconductor Manufacturing. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

Invest better with The Motley Fool. Get stock recommendations, portfolio guidance, and more from The Motley Fool’s premium services.

Making the world smarter, happier, and richer.

© 1995 – 2024 The Motley Fool. All rights reserved.

Market data powered by Xignite and Polygon.io.