3 Unstoppable Stocks to Buy With $400 Right Now – The Motley Fool

Founded in 1993, The Motley Fool is a financial services company dedicated to making the world smarter, happier, and richer. The Motley Fool reaches millions of people every month through our premium investing solutions, free guidance and market analysis on Fool.com, top-rated podcasts, and non-profit The Motley Fool Foundation.

Founded in 1993, The Motley Fool is a financial services company dedicated to making the world smarter, happier, and richer. The Motley Fool reaches millions of people every month through our premium investing solutions, free guidance and market analysis on Fool.com, top-rated podcasts, and non-profit The Motley Fool Foundation.

You’re reading a free article with opinions that may differ from The Motley Fool’s Premium Investing Services. Become a Motley Fool member today to get instant access to our top analyst recommendations, in-depth research, investing resources, and more. Learn More

Investors will find that the market is loaded with fantastic buys.

Although fractional shares are becoming more common, not everyone can access them. So, sometimes investors must be conscious of stock prices. Still, there are some incredible stocks that can be purchased for a fairly low dollar figure.

For just over $400, you can purchase a single share of Alphabet (GOOG -0.35%) (GOOGL -0.28%), Taiwan Semiconductor Manufacturing (TSM -3.18%), and CrowdStrike (CRWD 0.78%). But what makes these stocks buys right now? Read on to find out.

Alphabet is at the forefront of the artificial intelligence (AI) arms race. For years, it has been investing in building out its AI offerings by hiring engineers and developing products. However, the company seemed to have stumbled out of the gate when a few competitors beat it to the punch to launch some large language model products.

I don’t expect that to last forever just due to the sheer manpower Alphabet has on staff, which is a key catalyst for the stock’s future.

Furthermore, its primary revenue stream, advertising, hasn’t grown as quickly due to recessionary fears. If the economy can spin back into full gear, this revenue stream will open back up, and Alphabet will see tremendous growth. With the average analyst projecting 11% revenue growth in 2024, this thesis seems in line with what Wall Street expects.

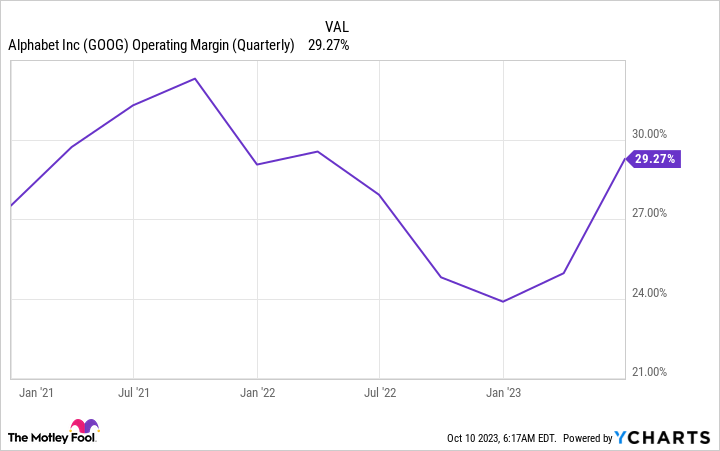

Alphabet has also been improving its operating margin, which was a concern when it went through its massive hiring spree.

GOOG Operating Margin (Quarterly) data by YCharts

With the outlook improving and margins rising, Alphabet looks like a no-brainer buy, trading around 25 times forward earnings.

Powering AI technology everywhere are chips from Taiwan Semiconductor Manufacturing. It’s the largest contract chip manufacturer globally and makes chips for giants like Apple and Nvidia. Although the business is currently hampered by weak demand for consumer electronics, that’s only a cyclical trend. Eventually, those devices will wear out, or a new one will be launched, creating further demand for the product.

The next iteration of chip technology, 3 nanometer (nm) chips, is almost here, which will drive much of this demand. These chips significantly improve over the current most powerful chip, 5 nm.

Although Taiwan Semiconductor has posted a few straight quarters of falling revenue (thanks to weaker demand), that trend isn’t expected in 2024. Wall Street analysts expect an impressive 23% revenue growth, which will be a major catalyst for the stock.

Additionally, the stock trades at 18 times forward earnings versus the S&P 500‘s 19 times, making it cheaper than most of the market. This doesn’t make sense, considering how crucial Taiwan Semiconductor is to the digital future, which is why I think it’s an outstanding buy right now.

Rounding out this list is the biggest growth company of the trio, CrowdStrike. CrowdStrike offers cybersecurity software in a cloud-first approach that protects network endpoints like laptops and cloud workloads. With cyberattacks becoming more prevalent, there has never been a more critical time to upgrade defenses than now, and CrowdStrike is primed to benefit from this move.

While many software companies have seen significant slowdowns during 2023, CrowdStrike hasn’t. In the second quarter of fiscal year 2024 (ending July 31), CrowdStrike’s annual recurring revenue rose 37% to $2.93 billion. Furthermore, it has posted a small net income profit each quarter in FY 2024, showing its resolution to become a profitable business.

Still, the company is difficult to value since it isn’t fully profitable. Instead, I’ll use a price-to-free cash flow (FCF) metric to value the stock, as FCF is an alternative profitability measure, especially if a company uses a lot of stock-based compensation (although there are some dangers to that application). From that standpoint, CrowdStrike trades at a pricey 54 times FCF, which may concern some investors.

However, with Wall Street analysts projecting 29% growth next year, this valuation will come down as CrowdStrike boosts profit and grows. CrowdStrike is at the forefront of a multiyear cybersecurity growth trend, and investors need some exposure to this incredible industry.

Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool’s board of directors. Keithen Drury has positions in Alphabet, CrowdStrike, and Taiwan Semiconductor Manufacturing. The Motley Fool has positions in and recommends Alphabet, Apple, CrowdStrike, Nvidia, and Taiwan Semiconductor Manufacturing. The Motley Fool has a disclosure policy.

Invest better with The Motley Fool. Get stock recommendations, portfolio guidance, and more from The Motley Fool’s premium services.

Making the world smarter, happier, and richer.

© 1995 – 2024 The Motley Fool. All rights reserved.

Market data powered by Xignite and Polygon.io.