1 Cheap Dividend Chip Stock With Big Upside From AI and Electric Vehicles – The Motley Fool

Founded in 1993, The Motley Fool is a financial services company dedicated to making the world smarter, happier, and richer. The Motley Fool reaches millions of people every month through our premium investing solutions, free guidance and market analysis on Fool.com, top-rated podcasts, and non-profit The Motley Fool Foundation.

Founded in 1993, The Motley Fool is a financial services company dedicated to making the world smarter, happier, and richer. The Motley Fool reaches millions of people every month through our premium investing solutions, free guidance and market analysis on Fool.com, top-rated podcasts, and non-profit The Motley Fool Foundation.

You’re reading a free article with opinions that may differ from The Motley Fool’s Premium Investing Services. Become a Motley Fool member today to get instant access to our top analyst recommendations, in-depth research, investing resources, and more. Learn More

KLA is well positioned as a new growth cycle begins for semiconductors.

Shares of semiconductor-manufacturing equipment company KLA (KLAC 1.82%) have been a top-notch investment, with the stock soaring to new all-time highs this year. And it remains near those levels as it has been a more stable business amid a nasty downturn for the semiconductor industry overall. A healthy dose of growing dividends and stock repurchases have kept investors’ interested.

Though it might not seem like it now, a new wave of chip demand is gearing up, driven by AI and electrification and digitization of vehicles, with KLA ready to capitalize on the trend. Here’s why this could be a great dividend-stock value for the long haul.

KLA is one of the “fab five” — the five specialist companies that dominate the market for equipment to make semiconductor wafers. In particular, the company dominates the metrology (the science of measuring stuff), process control, and diagnostics part of this niche. This equipment is especially important for quality control when a new chip manufacturing line fires up.

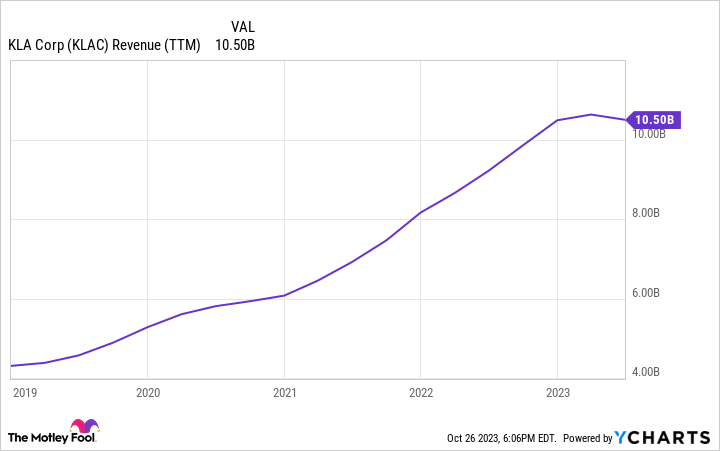

Given ongoing worries over global economic health, a big cyclical downturn for the chip industry (driven by a sharp fall from pandemic-era PC and smartphone sales), and businesses prioritizing cash conservation, the fab equipment market is down quite a bit in 2023. KLA has been holding on to most of its gains from the last few years, though.

Data by YCharts. TTM = trailing 12 months.

The reason for KLA’s outperformance is straightforward. While the company does sell equipment to parts of the industry affected by the chip downturn, it also is benefiting this year from trends in more mature markets like industrial applications and automobiles.

Cars are going electric and being equipped with lots more digital features, as is industrial equipment in fields like manufacturing, healthcare, and aerospace. All this means more new chips, which means more KLA equipment is needed to make sure those chips pass quality checks.

As for the big consumer electronics part of the industry that’s down and out, that market is bottoming out and should begin improving in 2024, led by a resumption of investments in more-advanced chips for new AI demand. And as the new wave of advanced chip manufacturing gathers force, KLA should report stronger sales and services once again.

Headed into the fiscal 2024 second quarter, things are already looking up. Management expects a sequential rise in revenue from $2.39 billion last quarter to $2.45 billion at the midpoint of guidance. Earnings per share under generally accepted accounting principles (GAAP) are also expected to rise from $5.41 last quarter to $5.54 at the midpoint in the fourth quarter. And there’s optimism that this trend will continue.

The real reason KLA is an attractive investment, though, is its consistent cash-return policy to shareholders. Before its latest earnings report at the end of October 2023, management announced another dividend increase (lifting the yield to 1.1%), and added $2 billion to the current share repurchase plan just over 3% of the company’s current market cap.

Image source: KLA Corp.

There’s lots of room to continue shelling out more cash, too. Free cash flow last quarter was $816 million, and quarterly dividend payments cost KLA just $182 million. This leaves lots of room for those stock buybacks, and for management to replenish the balance sheet as needed, which ended September 2023 with $3.35 billion in cash and short-term investments and debt of $5.89 billion.

Regardless of the trajectory of the fab equipment market in the coming quarters, the company’s profits could be poised to rise next year. After record sales the last two years during the chip shortage amid the pandemic (before the current cyclical slump), that equipment is about to begin exiting KLA’s two-year warranty and enter service contracts.

Services generated $560 million in sales last quarter (up 6% year over year), and management thinks it will accelerate to about 12% to 14% growth in 2024.

Outside of services, metrology and process-control equipment could remain a hot part of the semiconductor market over the next few years as tens of billions of dollars are poured into new chip fabs in the U.S., Europe, and Asia. This could play into the hands of KLA, as well as its tiny metrology peers Onto Innovation, Nova, and Camtek.

All in all, KLA has had a great run of growth, and it’s poised to build on that foundation as secular trends like EVs and AI heat up in the years ahead. At 19 times trailing-12-month earnings per share and 19 times free cash flow, this still looks like a top chip stock for investors looking for gradual growth and income.

Nicholas Rossolillo and his clients have positions in KLA and Onto Innovation. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.

Invest better with The Motley Fool. Get stock recommendations, portfolio guidance, and more from The Motley Fool’s premium services.

Making the world smarter, happier, and richer.

© 1995 – 2024 The Motley Fool. All rights reserved.

Market data powered by Xignite and Polygon.io.